Bank Loan Insurance vs Insurance Company Loan Insurance: A Complete Comparison Guide

Introduction

When borrowing money, protection against unexpected events is an aspect many borrowers consider alongside the loan itself. This protection often comes in the form of loan insurance, a financial product designed to support repayment if certain life circumstances affect the borrower’s ability to continue making payments.

Loan insurance may be offered directly through banks or provided by independent insurance companies. As a result, borrowers frequently encounter the question: Is bank loan insurance better, or is insurance company loan insurance a better choice?

The answer is not universal. Both options serve similar purposes but differ in structure, flexibility, accessibility, and overall borrower experience. Understanding these differences allows borrowers to evaluate options more effectively and align protection choices with their financial needs.

This article explores bank loan insurance and insurance company loan insurance in detail, compares their features, and provides practical examples using American names for clarity.

What Is Bank Loan Insurance?

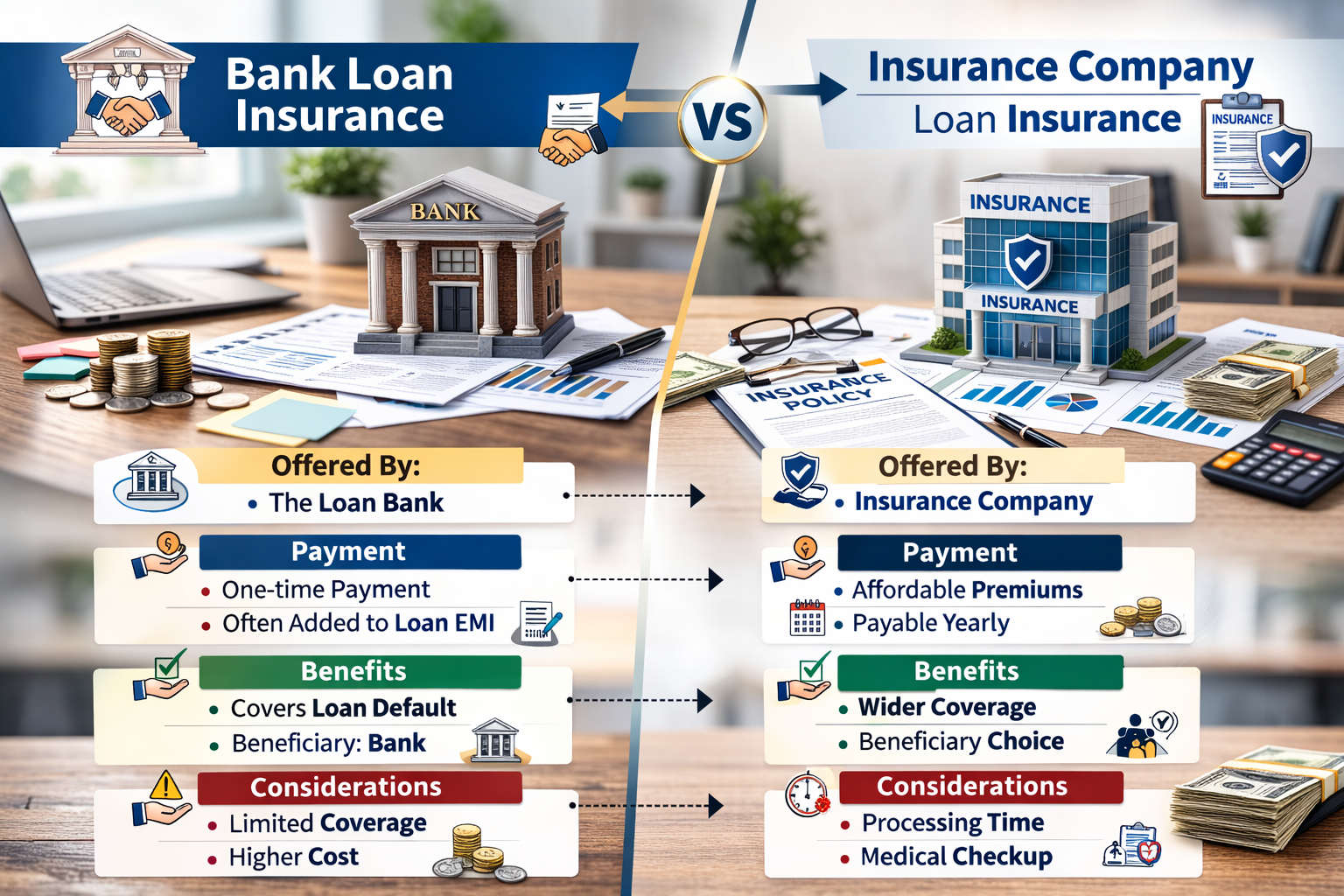

Bank loan insurance is coverage offered directly through a lending institution at the time of borrowing. It is typically linked to the loan account and integrated into the loan application process.

The primary objective is to protect loan repayment if the borrower experiences events such as death, disability, critical illness, or unemployment, depending on policy terms.

Key characteristics

-

Offered during loan application

-

Directly connected to the loan account

-

Claim payments often go straight to the lender

-

Administrative process handled through the bank

Example

Michael applies for a personal loan to fund home improvements. During the application process, the bank offers loan protection insurance.

Michael chooses the coverage, and the policy becomes associated with his loan account. If a covered event occurs, the insurer coordinates with the bank to manage repayment obligations.

This integrated structure illustrates how bank loan insurance operates within the lending framework.

What Is Insurance Company Loan Insurance?

Insurance company loan insurance refers to policies purchased independently from insurers rather than through the lender. These policies can still be used to protect loan repayment but are not embedded within the loan agreement.

Borrowers maintain greater autonomy in selecting coverage features and providers.

Key characteristics

-

Purchased separately from the loan

-

Greater customization options

-

Policy ownership remains with borrower

-

Benefits may be paid to borrower or lender

Example

Jessica obtains an auto loan from her bank but chooses to purchase loan protection coverage from an independent insurance provider.

When Jessica experiences a temporary disability, the insurer provides benefits according to her policy. She uses those benefits to continue loan payments.

This example demonstrates how insurance company loan insurance operates independently of the lender.

Similarities Between Bank and Insurance Company Loan Insurance

Despite structural differences, both options share common objectives.

Repayment protection

Both forms of coverage aim to support loan repayment during defined events.

Event-based activation

Coverage activates only under specified conditions outlined in policy documents.

Claim verification

Both require documentation and review before claim settlement.

Financial continuity

Each approach helps maintain loan account stability during challenging periods.

Recognizing these similarities prevents misunderstanding the fundamental purpose of loan insurance.

Key Differences Between Bank and Insurance Company Loan Insurance

1. Integration vs independence

Bank loan insurance is integrated into the lending process, while insurance company coverage exists independently.

2. Flexibility

Independent policies often allow broader customization in coverage features and duration.

3. Provider choice

Bank-linked insurance may involve limited provider options, whereas independent coverage allows comparison across insurers.

4. Claim flow

Bank insurance typically routes payments directly to lenders, while independent policies may provide benefits to borrowers.

5. Administrative experience

Bank insurance offers convenience through centralized management, while independent coverage may involve separate coordination.

Advantages of Bank Loan Insurance

Convenience

Enrollment occurs during the loan process, reducing additional steps.

Simplified coordination

Because the policy is linked to the loan, claim settlement often involves direct lender interaction.

Streamlined documentation

Borrowers typically submit fewer documents when enrolling through banks.

Structured integration

Loan and insurance data are maintained within a unified system.

Example

David takes a mortgage and accepts bank-offered loan insurance. Years later, when he experiences a covered event, the insurer coordinates directly with the bank, simplifying claim processing.

Advantages of Insurance Company Loan Insurance

Greater choice

Borrowers can compare multiple insurers and policy structures.

Customizable coverage

Independent policies may offer broader protection combinations.

Policy portability

Coverage may remain valid even if the borrower refinances or changes lenders.

Ownership clarity

Borrowers maintain direct control over policy terms and benefits.

Example

Emily finances education through a student loan but purchases independent loan insurance tailored to include disability and critical illness coverage. Later, when she refinances her loan with another lender, her insurance policy remains unaffected.

Situations Where Bank Loan Insurance May Be Suitable

-

Borrowers seeking convenience and simplicity

-

Individuals preferring integrated financial management

-

Borrowers with limited time for comparison shopping

-

Loans requiring fast approval processes

In these cases, embedded insurance may align with borrower priorities.

Situations Where Insurance Company Loan Insurance May Be Suitable

-

Borrowers wanting provider comparison

-

Individuals seeking customized coverage features

-

Borrowers anticipating loan refinancing

-

Those preferring independent financial planning

Here, flexibility and autonomy may be valued.

Real-Life Comparison Example

Bank insurance scenario

Robert obtains a home loan and enrolls in bank-provided mortgage protection insurance. The policy integrates seamlessly with his loan account, simplifying administration.

Insurance company scenario

Amanda takes a similar mortgage but purchases coverage from an independent insurer offering broader disability protection. Her policy remains separate from the lender.

Both borrowers achieve repayment protection, but their experiences differ in structure and flexibility.

Factors to Consider When Comparing Options

Convenience vs flexibility

Some borrowers prioritize ease, while others value customization.

Policy features

Coverage scope varies across providers and products.

Loan duration

Longer loans may influence preference for portable coverage.

Financial planning approach

Integrated vs independent management styles shape decisions.

Claim experience

Understanding how claims are processed supports informed expectations.

Common Misconceptions

“Bank insurance is always better”

Effectiveness depends on borrower preferences rather than a universal standard.

“Independent insurance complicates claims”

Many insurers offer streamlined claim processes comparable to bank-linked coverage.

“You must choose one permanently”

Borrowers may adjust insurance strategies as financial circumstances evolve.